All Categories

Featured

Table of Contents

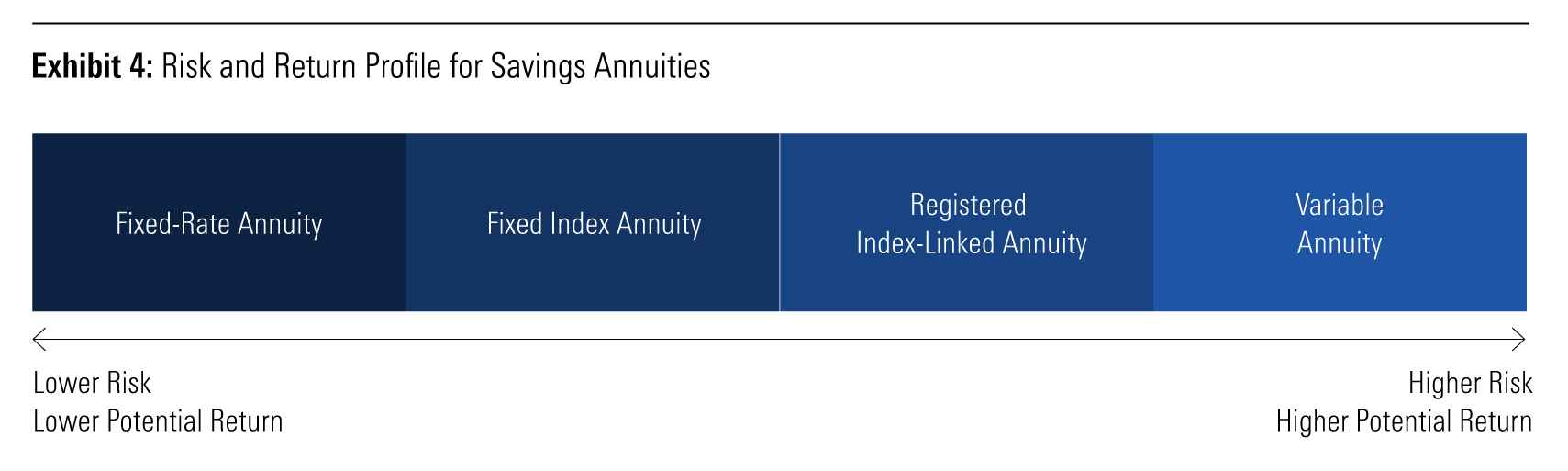

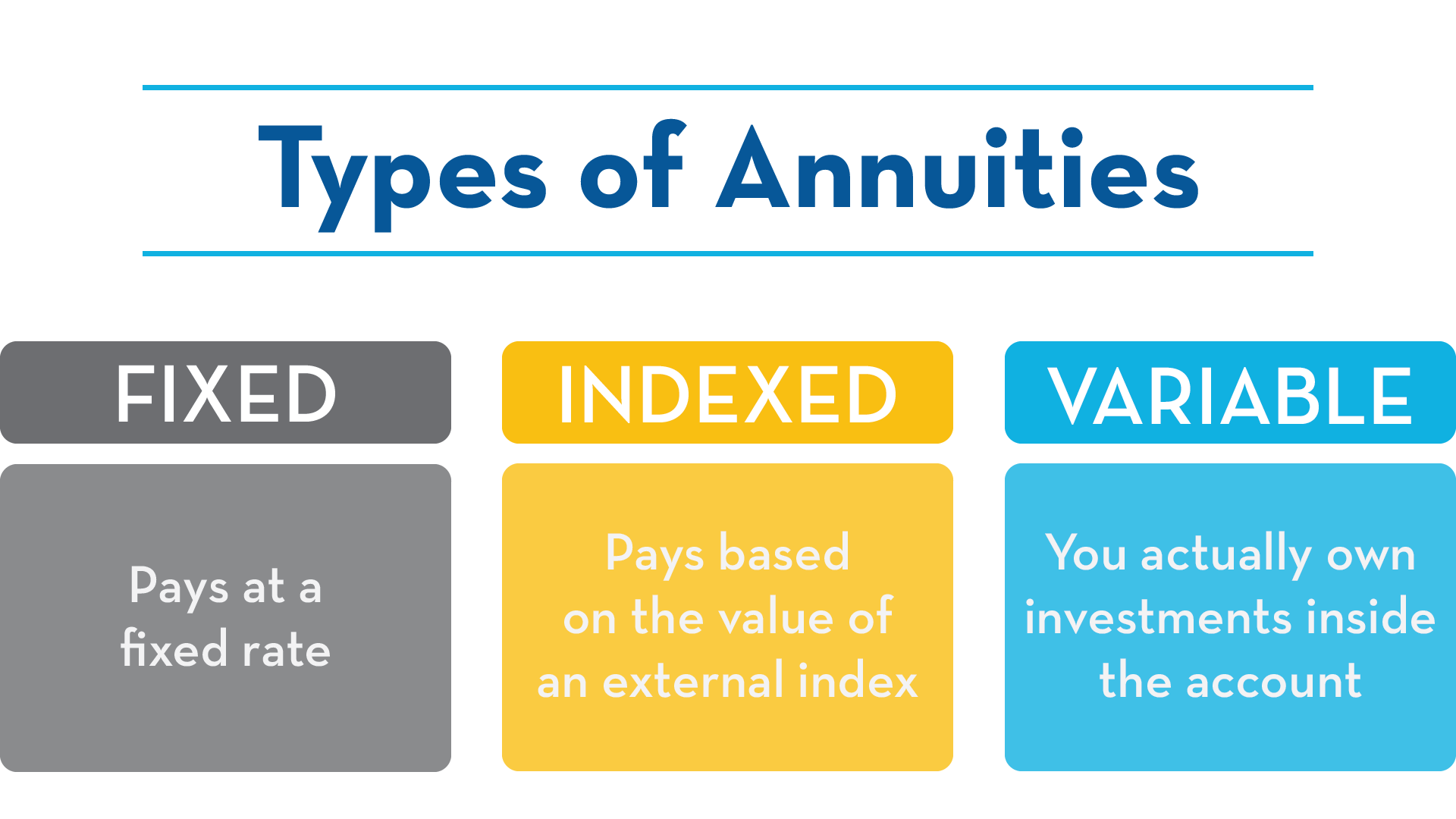

There are 3 kinds of annuities: fixed, variable and indexed. With a dealt with annuity, the insurance company ensures both the rate of return (the interest price) and the payout to the investor.

With a deferred fixed annuity, the insurance coverage company consents to pay you no much less than a specified price of rate of interest as your account is expanding. With an instant fixed annuityor when you "annuitize" your postponed annuityyou get a predetermined fixed amount of money, usually on a regular monthly basis (comparable to a pension plan).

While a variable annuity has the advantage of tax-deferred development, its yearly expenditures are most likely to be much more than the costs of a normal shared fund. And, unlike a fixed annuity, variable annuities do not give any type of warranty that you'll gain a return on your financial investment. Instead, there's a risk that you might in fact shed money.

Exploring Fixed Annuity Vs Variable Annuity A Closer Look at How Retirement Planning Works Defining the Right Financial Strategy Features of Annuities Fixed Vs Variable Why Variable Annuities Vs Fixed Annuities Can Impact Your Future How to Compare Different Investment Plans: How It Works Key Differences Between Tax Benefits Of Fixed Vs Variable Annuities Understanding the Rewards of Fixed Annuity Vs Variable Annuity Who Should Consider Annuity Fixed Vs Variable? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to What Is A Variable Annuity Vs A Fixed Annuity A Closer Look at How to Build a Retirement Plan

Due to the complexity of variable annuities, they're a leading resource of investor issues to FINRA. Before buying a variable annuity, meticulously read the annuity's prospectus, and ask the individual marketing the annuity to describe every one of the product's features, riders, costs and constraints. You need to additionally know how your broker is being compensated, including whether they're obtaining a payment and, if so, how a lot.

Indexed annuities are complex financial tools that have attributes of both repaired and variable annuities. Indexed annuities typically supply a minimum surefire interest rate incorporated with a passion price linked to a market index. Several indexed annuities are tied to broad, widely known indexes like the S&P 500 Index. But some usage other indexes, including those that represent various other segments of the marketplace.

Understanding the functions of an indexed annuity can be complicated. There are a number of indexing techniques companies utilize to calculate gains and, due to the variety and intricacy of the methods used to credit scores interest, it's challenging to compare one indexed annuity to another. Indexed annuities are usually categorized as one of the following two types: EIAs provide a guaranteed minimum rates of interest (typically a minimum of 87.5 percent of the premium paid at 1 to 3 percent rate of interest), in addition to an extra rates of interest linked to the performance of several market index.

With variable annuities, you can spend in a selection of safeties including stock and bond funds. Stock market performance establishes the annuity's worth and the return you will obtain from the cash you spend.

Comfortable with fluctuations in the stock exchange and desire your financial investments to equal rising cost of living over a long duration of time. Youthful and intend to prepare economically for retired life by reaping the gains in the supply or bond market over the long-term.

As you're constructing up your retirement savings, there are lots of ways to extend your cash. can be particularly valuable savings devices because they assure a revenue quantity for either a collection time period or for the rest of your life. Repaired and variable annuities are two alternatives that provide tax-deferred development on your contributionsthough they do it in various ways.

Decoding Variable Vs Fixed Annuity Key Insights on Your Financial Future Breaking Down the Basics of Investment Plans Benefits of Indexed Annuity Vs Fixed Annuity Why Variable Annuity Vs Fixed Indexed Annuity Can Impact Your Future Fixed Indexed Annuity Vs Market-variable Annuity: How It Works Key Differences Between Different Financial Strategies Understanding the Key Features of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing Retirement Income Fixed Vs Variable Annuity FAQs About Fixed Annuity Or Variable Annuity Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Tax Benefits Of Fixed Vs Variable Annuities A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

A supplies a guaranteed interest price. Your contract value will increase due to the amassing of guaranteed interest incomes, meaning it will not shed worth if the market experiences losses.

A consists of bought the securities market. Your variable annuity's financial investment performance will affect the size of your savings. It might assure you'll obtain a collection of payouts that start when you retire and can last the rest of your life, provided you annuitize (begin taking settlements). When you start taking annuity settlements, they will certainly rely on the annuity value back then.

Market losses likely will cause smaller payments. Any rate of interest or other gains in either sort of agreement are protected from current-year tax; your tax responsibility will come when withdrawals start. Allow's take a look at the core attributes of these annuities so you can choose how one or both might fit with your overall retired life strategy.

A set annuity's value will not decrease as a result of market lossesit's constant and stable. On the other hand, variable annuity values will rise and fall with the performance of the subaccounts you elect as the markets fluctuate. Incomes on your dealt with annuity will extremely rely on its acquired rate when bought.

Alternatively, payout on a fixed annuity acquired when rates of interest are low are most likely to pay earnings at a lower rate. If the rates of interest is ensured for the length of the agreement, profits will certainly stay continuous regardless of the markets or price task. A set price does not mean that fixed annuities are safe.

While you can't come down on a set rate with a variable annuity, you can pick to spend in conventional or aggressive funds tailored to your risk degree. Extra conservative investment choices, such as temporary mutual fund, can aid reduce volatility in your account. Because repaired annuities provide a set rate, dependent upon present rates of interest, they don't supply that same versatility.

Understanding What Is Variable Annuity Vs Fixed Annuity Everything You Need to Know About Financial Strategies Defining the Right Financial Strategy Advantages and Disadvantages of What Is A Variable Annuity Vs A Fixed Annuity Why Variable Annuity Vs Fixed Annuity Is Worth Considering How to Compare Different Investment Plans: How It Works Key Differences Between Different Financial Strategies Understanding the Risks of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing Fixed Interest Annuity Vs Variable Investment Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing What Is Variable Annuity Vs Fixed Annuity Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at Fixed Index Annuity Vs Variable Annuities

Of the its assured development from accumulated rate of interest repayments attracts attention. Dealt with rate of interest offer small development in exchange for their assured revenues. You possibly could make extra lengthy term by taking extra threat with a variable annuity, yet you might additionally shed cash. While repaired annuity agreements prevent market threat, their compromise is much less growth capacity.

Spending your variable annuity in equity funds will certainly supply even more potential for gains. The costs linked with variable annuities may be higher than for various other annuities. Investment options, death advantages, and optional benefit guarantees that might grow your properties, additionally add price. It's necessary to review functions and associated costs to make sure that you're not spending greater than you need to.

The insurance business might impose surrender fees, and the Internal revenue service might levy an early withdrawal tax obligation penalty. They start at a specific portion and then decline over time.

Annuity earnings go through a 10% very early withdrawal tax obligation fine if taken prior to you get to age 59 unless an exception uses. This is imposed by the IRS and puts on all annuities. Both taken care of and variable annuities give choices for annuitizing your equilibrium and transforming it into an ensured stream of life time earnings.

Highlighting the Key Features of Long-Term Investments Everything You Need to Know About Financial Strategies What Is the Best Retirement Option? Features of Smart Investment Choices Why Choosing the Right Financial Strategy Is a Smart Choice Deferred Annuity Vs Variable Annuity: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Key Features of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Choosing Between Fixed Annuity And Variable Annuity Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding What Is Variable Annuity Vs Fixed Annuity A Beginner’s Guide to Tax Benefits Of Fixed Vs Variable Annuities A Closer Look at Fixed Annuity Vs Variable Annuity

You might choose to utilize both taken care of and variable annuities. But if you're selecting one over the other, the differences matter: A may be a far better option than a variable annuity if you have an extra traditional danger tolerance and you seek predictable interest and primary security. A might be a far better alternative if you have a higher risk tolerance and want the possibility for long-term market-based development.

Annuities are agreements offered by insurance provider that assure the purchaser a future payout in routine installations, normally regular monthly and usually permanently. There are different sorts of annuities that are made to serve different objectives. Returns can be fixed or variable, and payments can be instant or deferred. A set annuity assurances payment of a collection amount for the term of the contract.

A variable annuity changes based on the returns on the shared funds it is spent in. A prompt annuity begins paying out as soon as the purchaser makes a lump-sum payment to the insurance provider.

Annuities' returns can be either repaired or variable. With a fixed annuity, the insurance firm ensures the purchaser a specific repayment at some future date.

{kind=link}

Table of Contents

Latest Posts

Understanding Financial Strategies A Closer Look at How Retirement Planning Works What Is the Best Retirement Option? Benefits of Immediate Fixed Annuity Vs Variable Annuity Why Choosing the Right Fin

Exploring Fixed Vs Variable Annuity Pros Cons A Comprehensive Guide to Fixed Indexed Annuity Vs Market-variable Annuity Breaking Down the Basics of Retirement Income Fixed Vs Variable Annuity Pros and

Decoding Fixed Vs Variable Annuity Pros Cons A Closer Look at How Retirement Planning Works Breaking Down the Basics of Investment Plans Features of Smart Investment Choices Why Fixed Annuity Vs Equit

More

Latest Posts